In June 2021, the collapse of Champlain Towers South in Surfside, Florida, killed 98 people. The association had been sitting on a $9 million repair backlog it couldn't afford to address. That tragedy is the extreme end of a question every board faces sooner or later: how much should a condo association have in reserves? The short answer is that you need to hit 70% to 100% of what a professional reserve study says you need. The real answer depends on your building's age, amenities, and the useful life of everything you maintain. This article walks through the benchmarks, the funding math, and how to check whether your community is actually prepared or just hoping the roof holds.

Key Takeaways

- How much a condo association should have in reserves depends on achieving 70% to 100% of the fully funded balance set by a professional reserve study.

- Reserves below 30% of the fully funded balance signal elevated risk of special assessments and deferred maintenance.

- Most associations allocate 20% to 40% of total assessments to reserves, and federal mortgage rules require at least 10% of the annual budget.

- Underfunded reserves can block buyers from securing Fannie Mae and Freddie Mac loans, dragging down property values.

- A reserve study is the foundation for accurate funding, mapping each component's useful life and replacement cost so boards aren't guessing.

What a condo/HOA reserve fund is and its purpose

A reserve fund is the pot of money a condominium association sets aside for major repairs and replacements of shared community assets. That means roofs, elevators, pavement, siding, pools, and the mechanical systems that keep the building running. It is separate from the money used to pay for landscaping, insurance, and utilities every month. The whole point of a condo reserve fund is to spread the cost of big, predictable expenses over the years. That way a $400,000 roof replacement doesn't land on owners all at once.

Here's the hard truth: reserves are not optional savings. They are how boards avoid special assessments and keep community stability intact when a 25-year-old roof finally gives out. According to the Community Associations Institute's Best Practices report on reserve studies, a properly funded reserve is one of the strongest signs of a financially healthy association.

Many boards assume their operating budget can absorb a big repair by tightening spending elsewhere. In reality, deferred maintenance compounds. A leaking roof damages the units below it, and what could have been a planned expense becomes an emergency the association can't fund. The condo reserve fund exists precisely so that long-term financial planning replaces panic.

Operating budget vs. reserve budget

Boards get these two budgets confused all the time, and the confusion costs communities real money. The operating budget covers recurring, predictable costs: utilities, insurance premiums, landscaping contracts, management fees, and minor repairs. The reserve budget funds major repairs and replacements that occur every several years or decades. Mixing them is a classic mistake. Working from a step-by-step HOA budget template helps boards keep those two categories cleanly separated from the start.

When a board raids reserves to cover an operating shortfall, the reserve balance quietly erodes. No one notices until a component fails. Here's why it matters: your annual operating budget resets every year, but reserve contributions are meant to accumulate. Skip a year of reserve funding, and you've dug a hole that takes several years of catch-up contributions to fill.

A clean structure keeps reserve dollars in a separate account, ideally one that requires board approval to touch. Federal guidance from the U.S. Department of Housing and Urban Development on condominium project approval reinforces this separation as a condition for loan eligibility. Treat the reserve budget as untouchable for daily expenses. The operating budget handles the year-to-year. The reserve fund handles the future.

How much a condo should have in reserves (benchmarks and the 70% rule)

So, how much should a condo association have in reserves, in real terms? The industry benchmark ties reserve health to a metric called percent funded. It compares your actual reserve balance to the fully funded balance your reserve study calculates. An association at 100% has exactly what it should. At 0%, it has nothing set aside for aging components.

The widely used reserves rule of thumb: 70% funded or above is considered strong, 30% to 70% is fair but worth watching, and below 30% is a red flag for special assessments. The 70% threshold matters because associations above that line rarely need emergency assessments. Those below it face sharply higher risk. That's why 70% funded shows up again and again as the practical target boards aim for.

Many people assume a full reserve means a big pile of idle cash. In reality, healthy condo association reserves are money that's already spoken for by the replacement schedule. The rule of thumb for reserves isn't about hoarding. It's about matching your balance to what your building will actually need. If your condo reserve fund sits at 40% funded and your roof is due in three years, you have a funding problem, not a savings surplus.

Reserve studies and how they determine funding needs

A reserve study is the document that turns guesswork into a plan. A qualified reserve specialist inventories every shared component the association must eventually replace. They estimate the remaining useful life of each and project the future cost of replacement. From that inventory, the study calculates your fully funded balance and recommends a contribution schedule.

Without a reserve study, boards are guessing at reserve requirements, and that guesswork produces underfunded reserves. The study is the difference between "we think the roof has a few years left" and "the roof has seven years and will cost $380,000." That precision is what makes accurate condo association reserves possible.

Reserve studies come in tiers. A full study includes an on-site inspection. An update with a site visit refreshes an existing study. An update without a site visit adjusts the numbers based on reported conditions. Most associations should get a reserve study update every 1 to 3 years, with a full study every 3 to 5 years, depending on state reserve laws.

Reserve requirements and study frequency vary by jurisdiction. Florida's SIRS requirements, California's reserve study mandates, and Nevada's rules all differ. A guide to HOA reserve study requirements by state can help you identify which requirements may apply to your community. Check your state's condominium statute and consult your association attorney for interpretation before finalizing your capital planning.

Funding methodology: full, baseline, threshold, and underfunding

Choosing a funding methodology is one of the most important decisions a board makes, and most boards never realize they had a choice. There are four common approaches, and they produce very different contribution amounts.

Full funding aims to keep the reserve at or near 100% of the fully funded balance at all times. It costs the most per year but eliminates most special assessment risk. Baseline funding keeps the reserve balance above zero so cash is always available, but it allows the percent funded to drift lower, which raises risk. Threshold funding sets a target percentage funded, often around 70%, and provides funding to maintain that floor. It's a middle path between cost and safety. The fourth "method" isn't really a method at all: underfunding, where the board simply contributes less than any study recommends and hopes for the best.

The root cause of most reserve crises is a board defaulting into underfunding by keeping dues artificially low. Owners like low dues today. Then a $30,000-per-unit special assessment arrives, and community stability collapses along with owner trust. A deliberate funding methodology, chosen with the reserve study in hand, is how boards avoid that outcome.

Percentage of dues/budget to allocate to reserves

A common question from treasurers: what percentage of dues for reserves is right? Most well-run associations direct 20% to 40% of total assessments into their HOA reserve fund. The exact figure is driven by the reserve study rather than a flat rule. A brand-new building with young components might sit near the low end. An aging property with a failing roof and elevators may need to push past 40%.

There is one hard floor worth knowing. The FHA reserve requirement, along with Fannie Mae's 10% reserve funding guideline for condos and Freddie Mac guidelines, requires condo projects to allocate at least 10% of the annual operating budget to reserves to be loan-eligible. That 10% is a minimum for mortgage approval, not a target for reserve health. Treating the FHA reserve requirement as your goal is how communities end up underfunded.

The percentage of dues for reserves should be based on the numbers in your study, not on what feels affordable at the annual meeting. A board that sets dues for its HOA reserve fund based on the replacement schedule protects owners far better than one that sets dues low and prays. Long-term financial planning always beats a comfortable annual budget.

Factors that determine the right reserve amount (size, age, amenities, asset lifecycle)

No two associations need the same reserve balance, because no two share the same physical assets. Building age is the biggest driver. A 40-year-old high-rise with original plumbing and a roof at the end of its life needs far more in the bank than a five-year-old townhome community. As components age, their remaining useful life shrinks, and the funding pressure climbs.

Amenities matter just as much. A community with a pool, elevators, a clubhouse, private roads, and a fitness center carries a longer list of shared community assets to replace than one with landscaping and a parking lot. Every amenity is a future liability on the replacement schedule. More amenities mean more reserve requirements, full stop.

Size and structure play in too. A larger association spreads costs across more units, which can lower the per-unit burden, but it also multiplies the number of major repairs and replacements on the horizon. Construction type, climate, and quality of past maintenance all shift the asset lifecycle. Consider a coastal Florida condo where a board deferred a roof recoat two years in a row to keep dues flat: salt air accelerated wear, the roof failed early, and owners absorbed a special assessment that a funded reserve would have covered. This is why a reserve study built for your specific community always beats any generic reserves rule of thumb.

How to evaluate your community's reserve health/percent funded

Start with one number: percent funded. Divide your current reserve balance by the fully funded balance from your most recent study. If you're above 70%, your reserve health is solid. Between 30% and 70%, you're vulnerable to a bad year. Below 30%, a special assessment is likely a matter of when, not if.

But percent funded alone can mislead. A community might sit at 65% funded and still be fine if its major components are years away. Another at 65% with a roof due next spring is in trouble. Here's why it matters: percent funded is a snapshot, and the replacement schedule is the timeline. Read them together. Solid bookkeeping practices for small HOAs make it far easier to keep the balance figure accurate and up to date.

Also check whether your reserve study is current. A study from five years ago reflects five-year-old costs, and construction inflation has been brutal on major repairs. An outdated study can make underfunded reserves look healthier than they are. Pull your latest study, recalculate percent funded, compare it against upcoming replacements, and confirm your contribution rate is keeping pace. That's the honest picture of your condo association reserves.

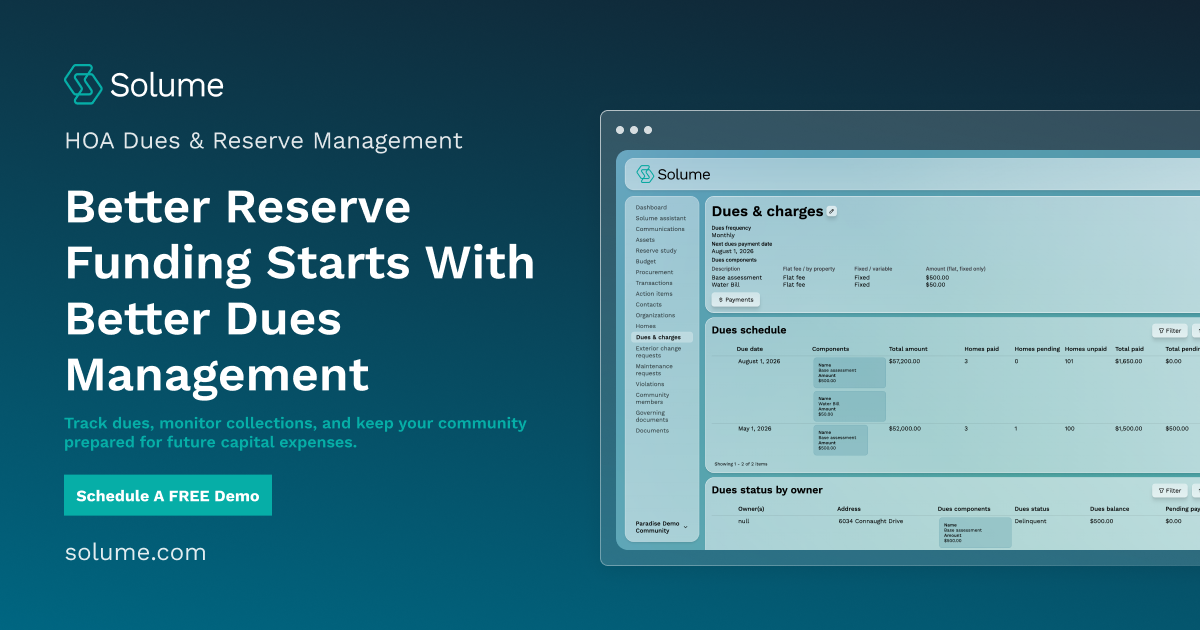

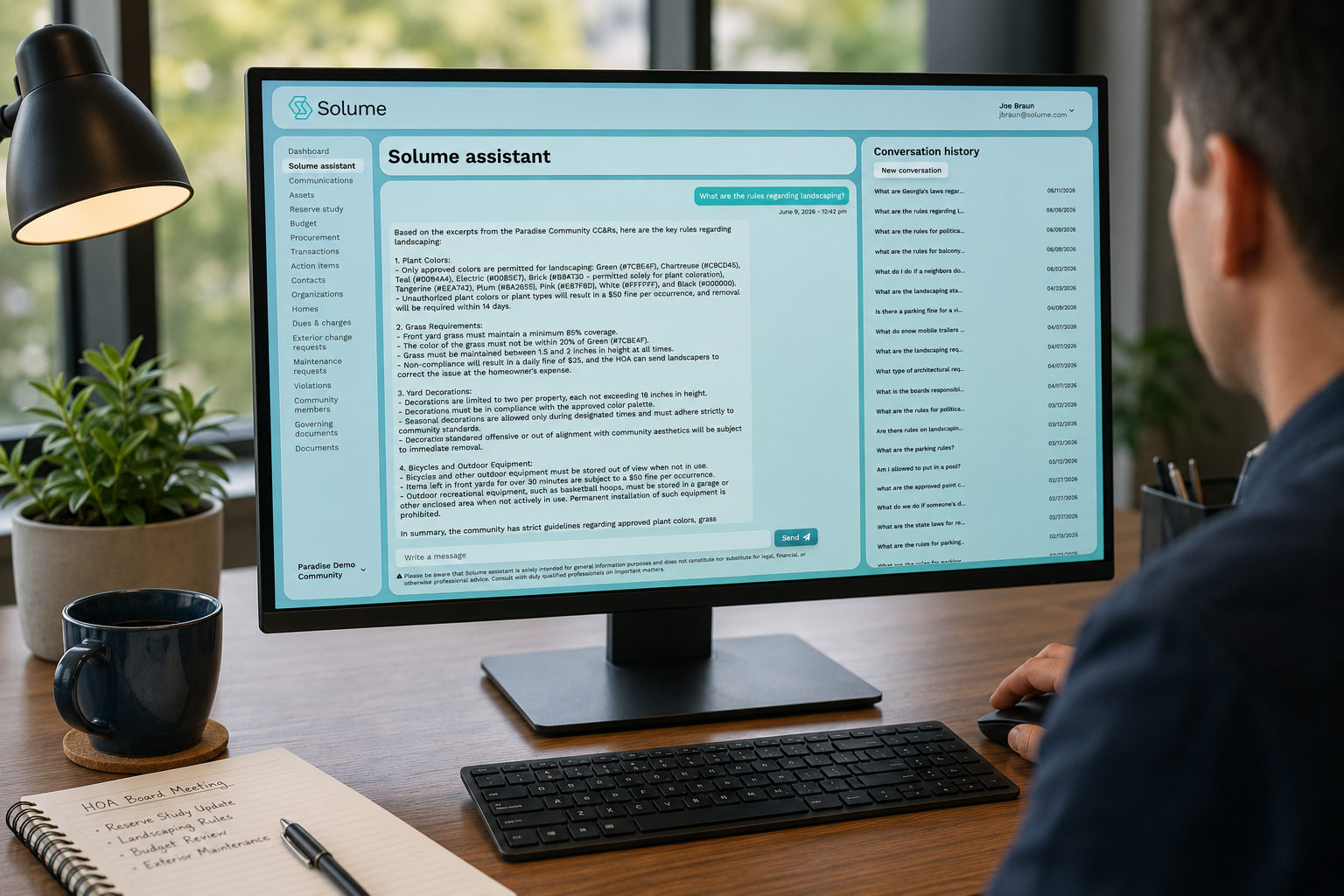

How reserve study software and automation help boards track reserves

Spreadsheets are where reserve tracking goes to die. A treasurer builds a beautiful workbook, then rotates off the board two years later. The next volunteer inherits a file no one understands. Reserve study software solves the continuity problem by keeping the component inventory, funding schedule, and current balance in one place that survives board turnover.

Automation also catches the drift that manual tracking misses. Reserve study software can flag when contributions fall behind schedule, update projections as costs change, and show percent funded in real time instead of once a year at budget season. For self-managed communities without a management company doing this work, that visibility is the difference between planning and reacting.

Solume's automated reserve study tool and compliance tracking are built for exactly this. They help self-managed communities keep their condo reserve fund aligned with state reserve laws and their replacement schedule without a full-time finance staff. Pairing that with financial management and reporting tool for budgeting and reporting gives volunteer treasurers strong visibility into capital planning to support their work.

Reserve transparency and fiduciary duty for volunteer boards

A board's fiduciary duty isn't an abstract legal phrase. It means the people running the condominium association are generally obligated to act in the community's financial interest. Underfunding reserves to keep dues low can breach that duty. Boards have been sued by owners who bought into a community, then got hit with an assessment the board saw coming and hid. In states like Florida, Florida Statute 718.112 on condominium reserves addresses much of this obligation, and Florida's strict condo reserve funding rules show how seriously legislators now take underfunding.

Financial transparency is how boards protect both the community and themselves. When owners can see the reserve study, the percent funded figure, and where their dues go, trust follows. Most boards assume owners will revolt over a dues increase. In reality, owners resent surprise special assessments far more than a transparent, well-explained plan tied to the HOA reserve fund.

Documenting the board's reasoning is part of board responsibility. If you're funding at threshold rather than full funding, write down why. States impose their own mandates too, such as California Civil Code Section 5550 reserve study requirements, so a documented rationale should reflect what your statute requires. If the reserve study recommends a dues increase and the board declines, record that decision and its rationale. That paper trail shows the board took its responsibilities seriously, which matters if a decision is ever questioned. Volunteer boards defend their choices by upholding fiduciary duty, financial transparency, and long-term planning. Confirm your specific obligations with your association attorney.

If your board wants a clearer way to handle reserve planning, financial transparency, and compliance without leaning on a management company, you can book a 15-minute call to see if Solume fits your community. It's built for self-managed boards that want to protect community stability and get ahead of special assessments rather than react to them.

Frequently Asked Questions

How much should a condo association have in reserves?

A well-funded condo reserve holds roughly 70% to 100% of the fully funded balance: the total needed to cover anticipated repairs and replacements of common elements over the next 20 to 30 years. A professional reserve study sets the precise target for your community, but falling below 70% is generally treated as underfunded.

What's the rule of thumb for HOA reserves?

As a general benchmark, associations should aim for a reserve fund that's 70% to 100% funded and allocate about 20% to 40% of total assessments toward reserves each year. Federal mortgage guidelines from Fannie Mae and Freddie Mac also require at least 10% of the annual budget to go to reserves.

How do you calculate the right reserve amount for your community?

Start with a professional reserve study that inventories every common-area component, estimates its remaining useful life, and projects replacement costs. From there, boards typically fund reserves using either the component (straight-line) method, which saves for each item individually, or the cash flow method, which manages the fund as a whole to maintain a minimum balance.

What happens to our condo values if reserves are underfunded?

When reserves dip below the minimum federal threshold, buyers may struggle to qualify for conventional Fannie Mae or Freddie Mac loans, shrinking the pool of eligible purchasers. Fewer qualified buyers and the looming threat of special assessments both put downward pressure on resale values.